Source page — copy text into Substack/LinkedIn, upload the visuals. noindex · not public

Closelook@Global Stock Markets · Weekly Edition

"Where the AI Dollar Actually Lands"

"Of every $100 the hyperscalers spend, about $35 reaches Asia — and inside the AI rack, memory and compute split three-quarters of the bill. This week the market listed direct access to the memory side."

Closelooknet is a reader-supported publication — to receive new posts and support the work, become a free or paid subscriber.

This week's edition of Closelook@Global Stock Markets, dated July 11, 2026.

Last week we showed you that the ex-US rally is six regions wearing a twenty-six-region costume — a concentrated AI-chip bet led by Taiwan and Korea. This week we follow the money to show why it looks that way: we trace what happens to every $100 the hyperscalers spend, how much of it lands in Asia, and which two buckets inside the AI rack take three-quarters of the bill. The market spent the week drawing the same map — and concluded by taking Korea's champion to New York.

1 · This Week's Action

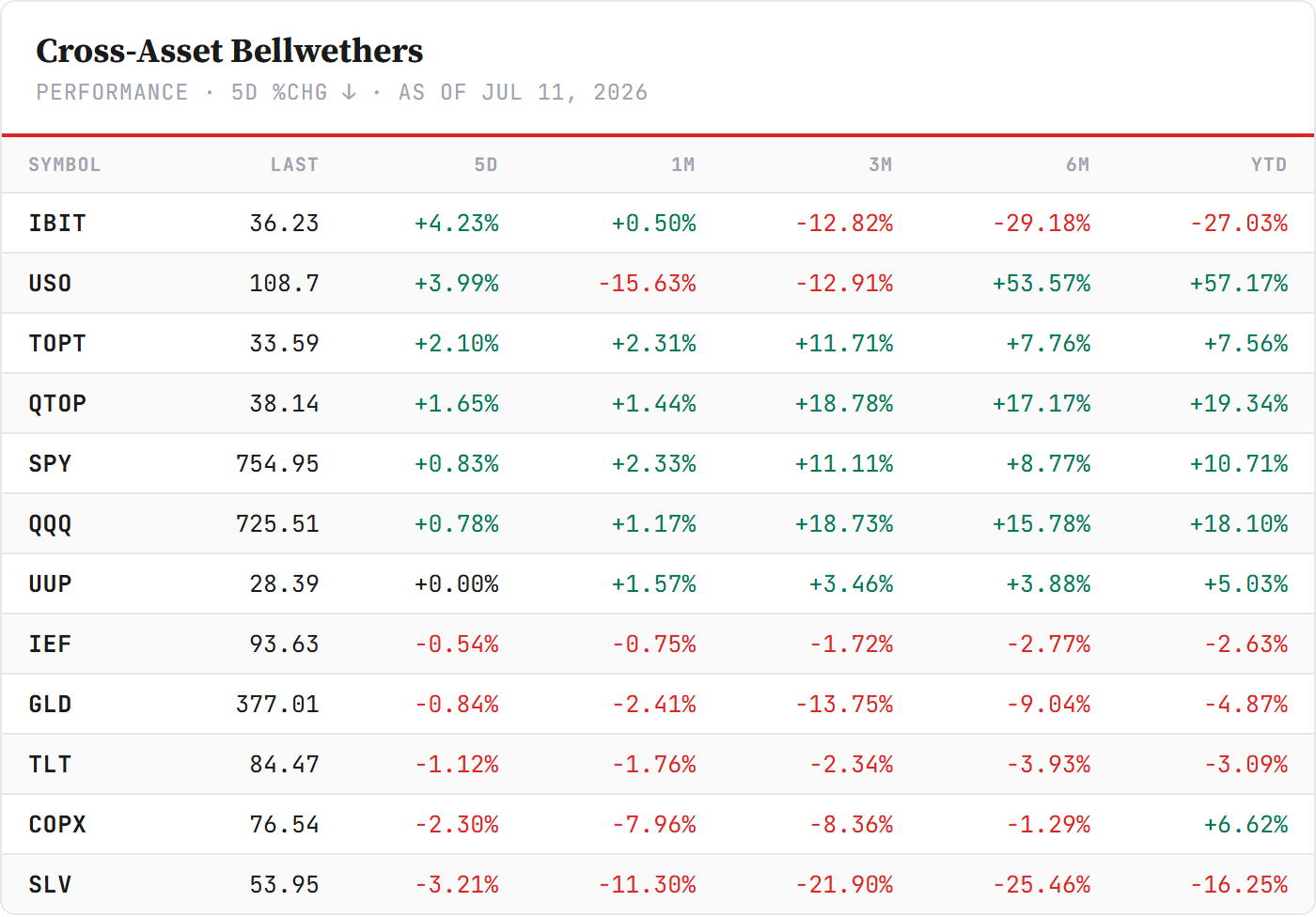

The cross-asset backdrop. The board reads risk-on with a commodity accent. Oil led the week (USO +4.0%, now +57% year-to-date) — the "oil isn't buying the war" read of recent weeks got at least a partial rebuttal. Bitcoin continued its repair (IBIT +4.2%), and the mega-cap concentrates outran the broad market (TOPT +2.1%, QTOP +1.7%, against SPY +0.8%). On the other side, gold eased 0.8% but held comfortably above the 4,000 belief line, and the long end sold off again (TLT −1.1%) after the hawkish minutes. The rates question is not resolved — it is just not this week's headline.

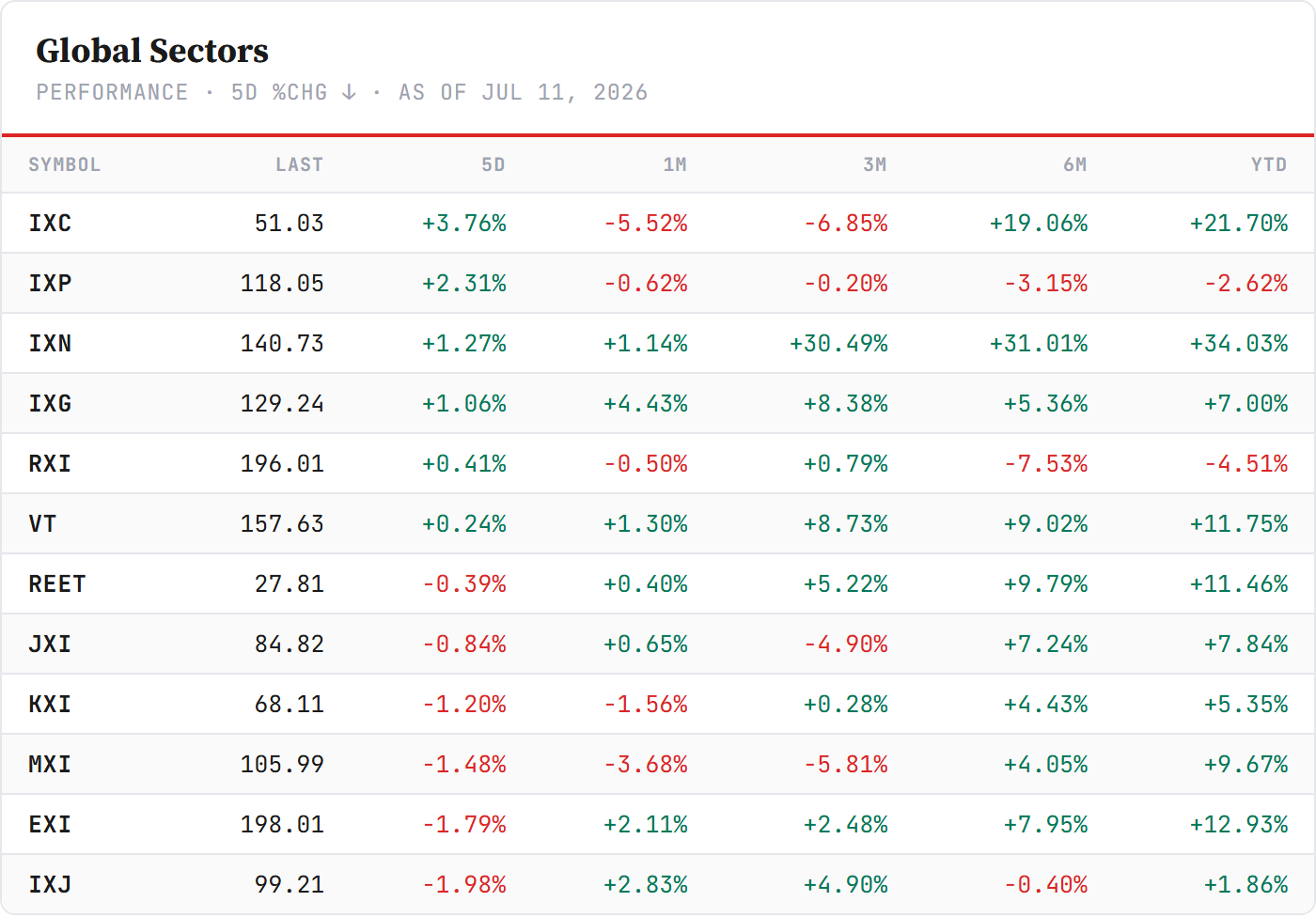

The global sectors. Energy led (+3.8%) as oil caught its bid, followed by telecom (+2.3%), tech (+1.3%) and financials (+1.1%) — while every classic defensive closed red: healthcare −2.0%, staples −1.2%, utilities −0.8%. That is a risk-on rotation inside a barely-moving global tape (VT +0.2% on the week).

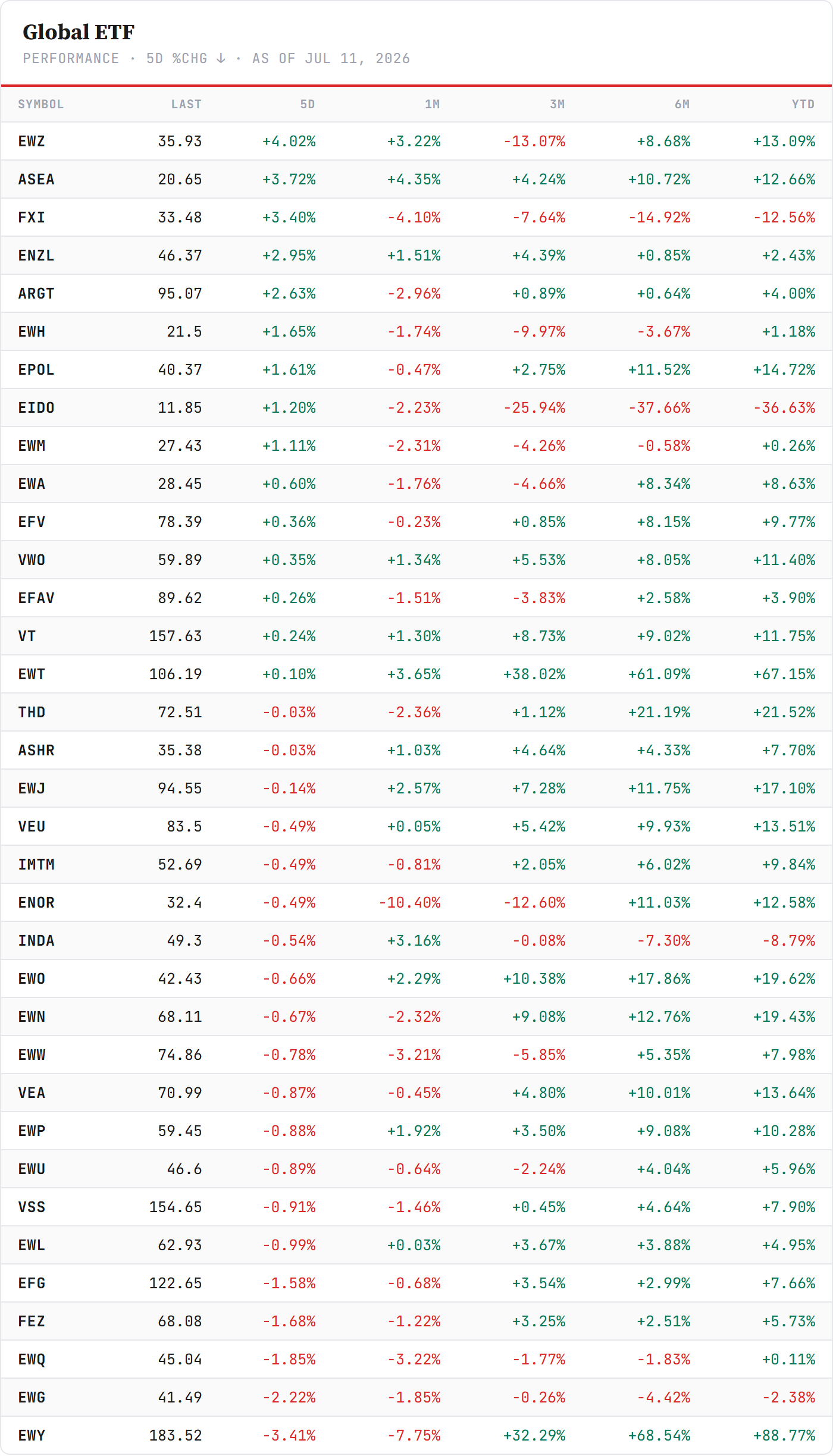

The regions. The board answers last week's question — and inverts it. We asked whether participation would broaden beyond the two chip countries. It did, but not the way a trend-follower would have guessed: the periphery led — Brazil +4.0%, Southeast Asia +3.7%, China +3.4%, New Zealand +3.0%, Argentina +2.6% — while Korea rested (EWY −3.4% after its +89% year-to-date run) and Taiwan sat flat. The year-to-date count moved from six regions beating VEU to seven; Poland joined the club. Breadth is broadening at the margin — one week, one region at a time.

2 · The State

The event of the week — the listing. The demand question got answered three times in one week. SK Hynix — the HBM leader and the cheapest large AI name in the world — sold $26.5 billion of ADRs in the largest US listing by a foreign company on record. The book was covered multiple times over. The deal priced at $149, a 2.9% premium to Seoul's close, where offerings of this size normally price at a discount. And when the ADRs opened on Nasdaq on Friday, the first trades printed near $170 — with an intraday high of $177 — before closing at $168.31, thirteen percent above the offer. The ticker converts from SKHYV to SKHY on Monday.

The tension worth naming. The same week the primary market paid up, the secondary market sold: Micron gave back part of its trillion-dollar week, and the memory complex traded red into the debut. That is not a contradiction — it reads like capital rotating from the expensive expression of the thesis (Micron at ~6.6x forward) into the cheaper new one (SK Hynix at ~4.8x at the offer, ~5.5x after the pop). The Korea discount is not closing by argument; it is closing by arbitrage.

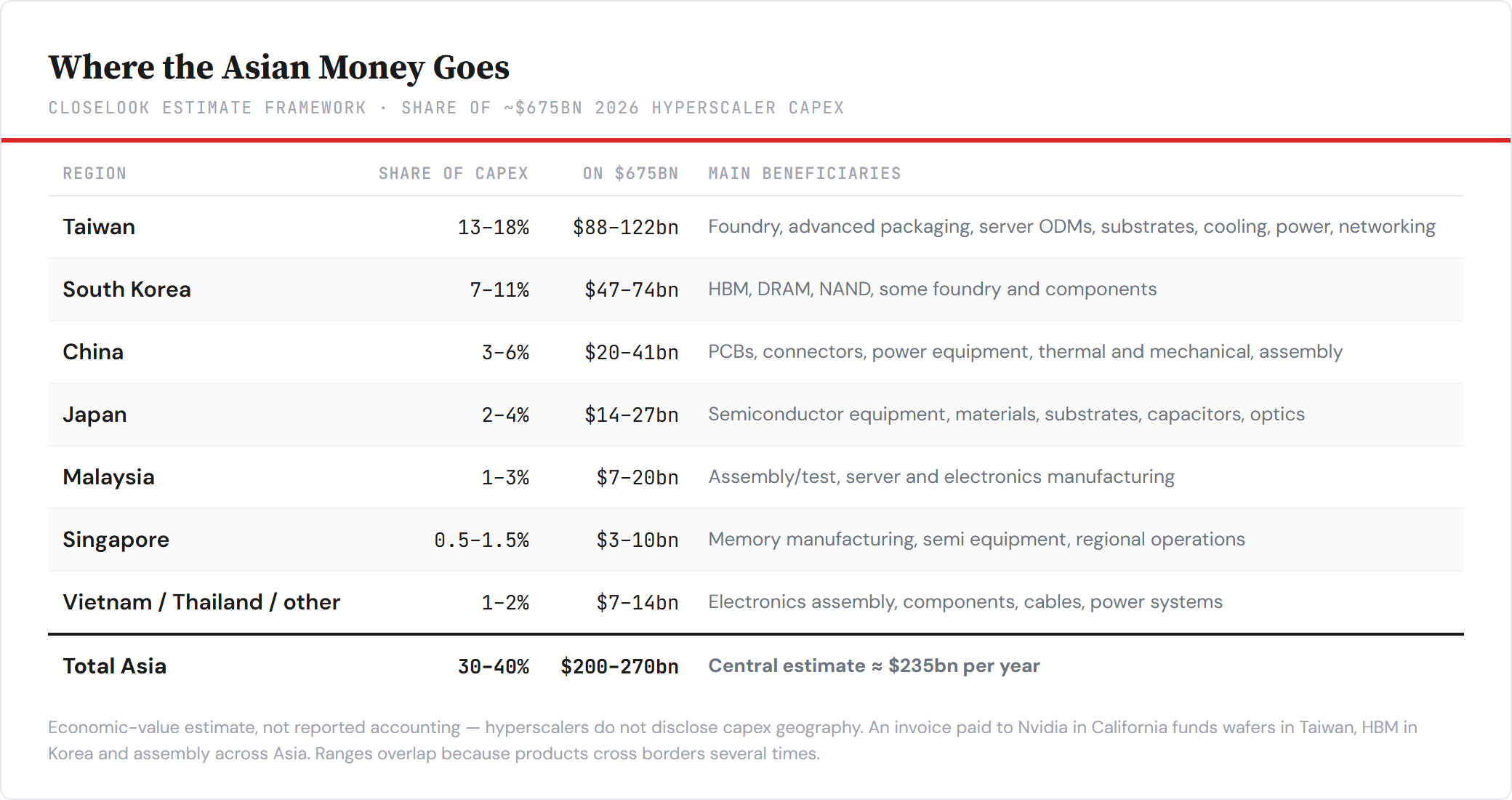

Follow the dollar. The listing is the visible end of a pipeline worth tracing in full. The four large US hyperscalers are heading toward roughly $650–700 billion of combined 2026 capex — Alphabet guides to $180–190 billion, Meta to $125–145 billion, and Microsoft says it is expanding AI capacity by more than 80% while roughly doubling its data-center footprint over two years. Our working estimate for where that money lands: of every $100, $45–55 stays in the US or wherever the data center is built, $10–20 goes to Europe, Mexico and other regions — and $30–40 ultimately accrues to Asian production and suppliers. For the incremental AI-compute dollar the Asian share is higher, around $40–50 of every $100, because the marginal AI dollar contains more GPUs, HBM, advanced packaging, server assembly and cooling — and less land and conventional construction. On a $675 billion midpoint, that implies an Asian revenue pool of roughly $200–270 billion a year, central estimate around $235 billion. This is an economic-value estimate, not a reported accounting number — hyperscalers do not disclose the geography of their capex, and an invoice paid to Nvidia in California ultimately funds wafers in Taiwan and HBM stacks in Korea.

Taiwan is the largest single destination — 13–18% of total capex, $88–122 billion across foundry, advanced packaging, server ODMs, substrates, cooling and power. Korea's share is narrower but more concentrated — 7–11%, $47–74 billion — because it flows almost entirely into the single most profitable bucket: memory. Korean producers supplied nearly four-fifths of global HBM revenue in the first quarter (SK Hynix 58%, Samsung 21%, per Counterpoint). Japan sits one or two layers upstream — equipment, wafers, photoresists, substrates — collecting its share when TSMC, SK Hynix and Samsung spend to expand. China's manufacturing footprint is larger than its profit capture. Malaysia and the rest of Southeast Asia are the China-plus-one winners.

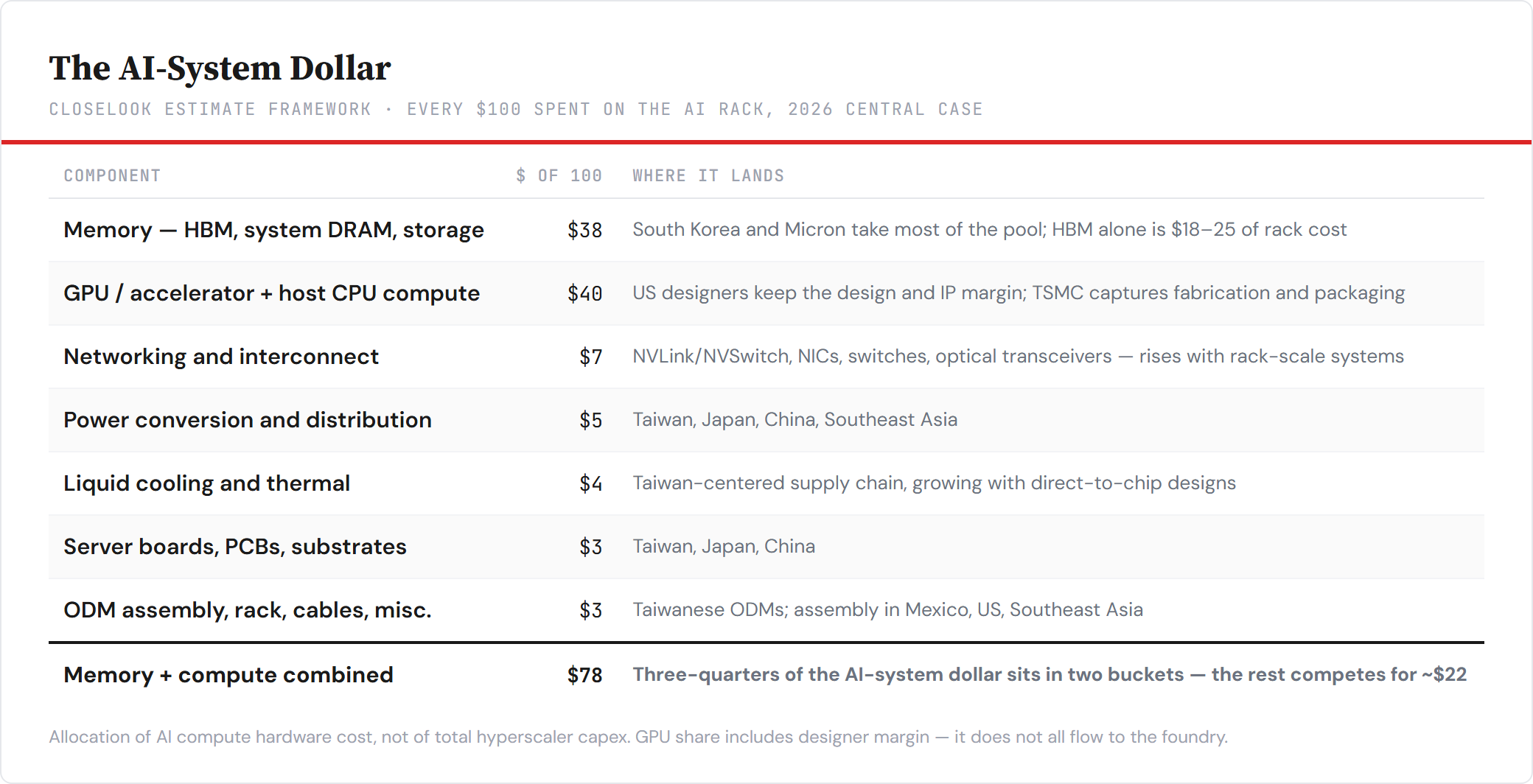

Inside the AI rack. Cut the same $100 differently — not hyperscaler capex, but the AI system itself — and the concentration sharpens further. Our 2026 central case: memory takes $38 of every AI-hardware $100 (HBM alone is $18–25 of complete rack cost), accelerator and host-CPU compute takes $40 (with the design and IP margin staying largely in the US, and TSMC capturing the fabrication and packaging slice), and everything else — networking, power, cooling, boards, assembly — competes for the remaining $22.

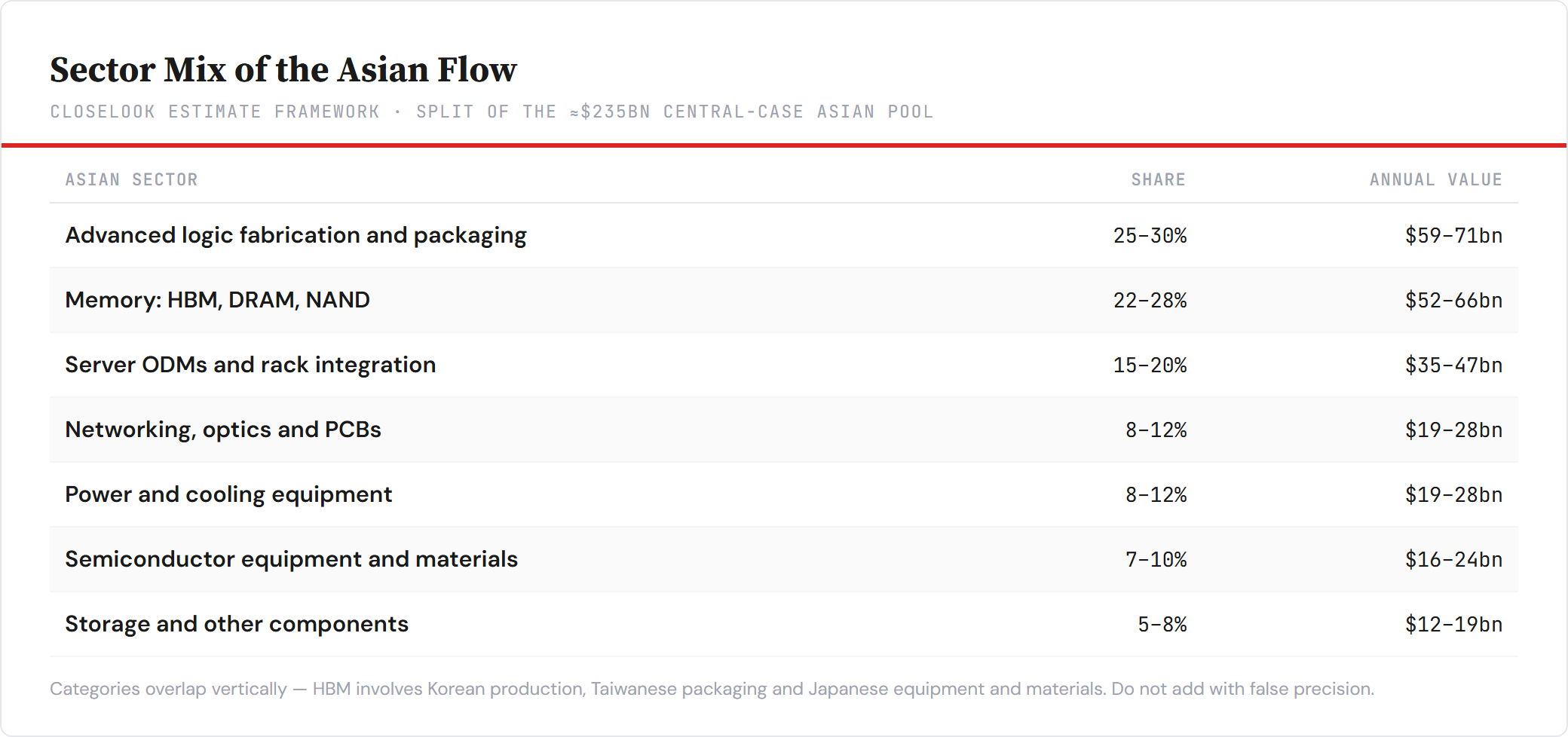

Memory and compute now divide roughly three-quarters of the AI-system dollar between them. That is why the economic leverage sits with HBM suppliers, accelerator designers and advanced-packaging capacity rather than with conventional server assemblers — and why the memory story keeps forcing itself into this letter. Within the Asian pool itself, the two largest slices are advanced logic fabrication with packaging, and memory:

The concentration check, week two. The Vanguard four-slice comparison keeps score on the same story from the top down: VEU (large-cap tilted, chip-heavy at the top) finished Friday at +14.2% year-to-date against VSS (small-caps, no mega-cap chip names) at +8.5% — the gap widened to 5.7 points from five a week ago. The rally is still being carried by exactly the names the flow framework says are collecting the capex dollar.

The two legs against each other. Taiwan compounded steadily all year; Korea went vertical from May. This week the two swapped character — Taiwan flat, Korea digesting. That is what a hand-off inside a theme looks like, not a top.

The structural read. The long view keeps the story honest. The red ascending channel drawn from the spring low is intact, with price riding its upper half into Friday's close — every correction since has held inside the rails, including April's fast flush. VEU trades above all three of its moving averages (the 200-day is the purple line far below the channel), and our chart terminal's machine wave read (beta) counts the advance as an impulse now in a fifth-wave extension, with invalidation far beneath the market at 52.54. Nothing in the structure argues against the trend — the risk at this altitude is breadth and rate path, not pattern.

3 · The Outlook

The four indices. The week told the whipsaw story honestly. Rubin fell 5.6% on Tuesday, recovered 3.9% on Thursday — the first all-green day since Monday — and finished the week at −0.1%: a round trip. The agentic side led into Thursday and then gave back 3.3% on Friday, into the debut, ending the week at +1.4% (AEI). AW40 added +1.7%, HALO lost −2.6%. Year-to-date the ladder reads: Rubin +119%, AEI +47%, HALO +5%, AW40 −21% (equal-weight variants). The barbell swapped sides twice and ended the week close to balance — this is a tug-of-war, not a regime change. Friday's give-back on the agentic side is the same rotation §2 describes: capital moving toward the cheaper expressions of the same theme.

4 · What May Lie Ahead

Support, resistance and the levels that matter. VEU closed at 83.50 — 1.1% above its 50-day average (82.6) and 2.7% below its 52-week high (85.74). The channel read stays constructive as long as pullbacks hold the 50-day shelf. The new line on the map is $149 — SK Hynix's offer price; that is the level below which the debut narrative would flip from demand-proof to fade. The concentration levels themselves rotated this week: Korea now sits about 3% below its 50-day after the rest week, while Taiwan holds 6% above its own — the leaders, not the laggards, are the charts that need to prove the pause is rotation, not distribution.

Divergences worth watching. The breadth question got a partial yes: seven of twenty-six regions now beat VEU year-to-date, and this week's leadership came from the periphery — Brazil, Southeast Asia, China. If the laggards' week becomes the laggards' month, the ex-US bull broadens into something sturdier than a two-country bet. If it doesn't, the divergence simply moves house: from "nobody participates" to "the leaders stopped."

The regime backdrop. Money Temperature composite at 54 — neutral-risk-on, a touch warmer than last week, in character unchanged: enough heat to fund rotation, not enough to signal euphoria.

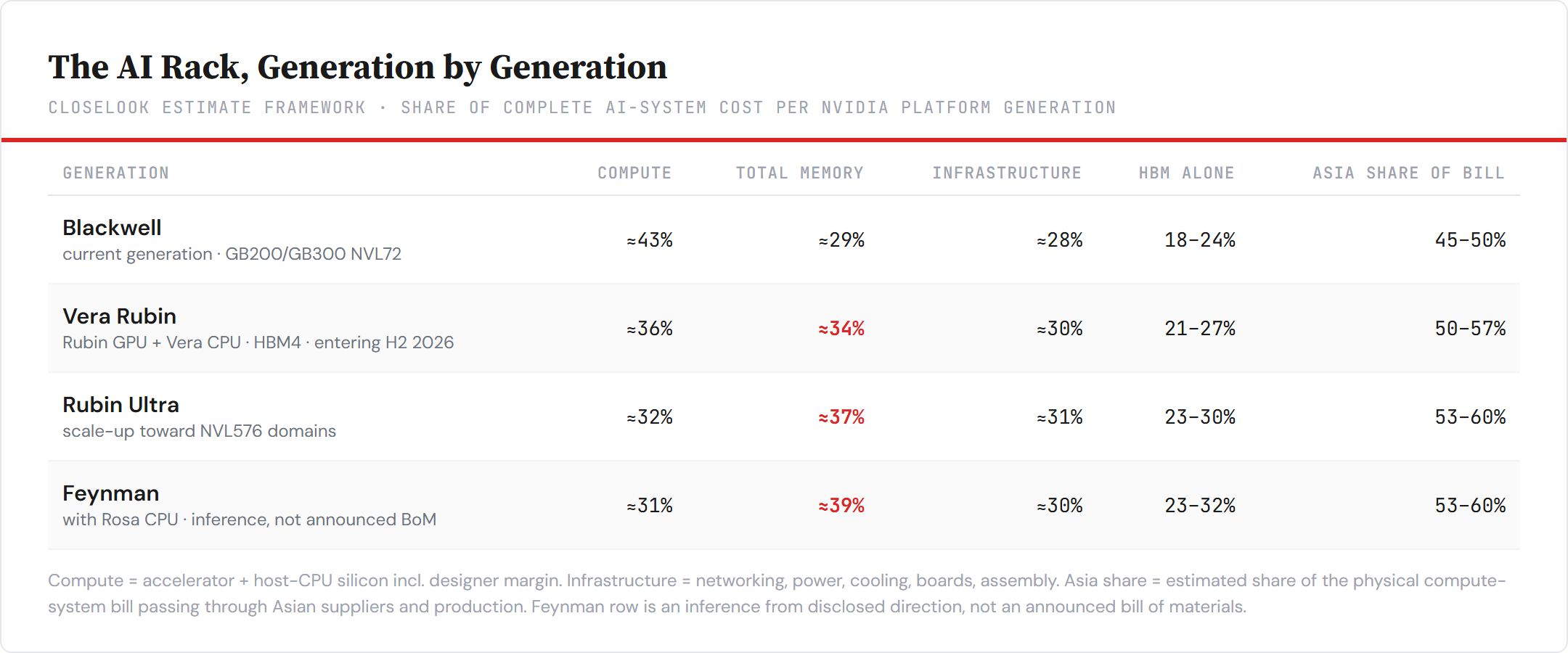

The next racks tilt the dollar further. Nvidia's roadmap gives the flow framework its forward path — with a naming note for clarity, since the generations are often garbled: Blackwell is the current generation; the next platform is Vera Rubin (the Rubin GPU paired with the Vera CPU, entering the market in the second half of this year); Rubin Ultra scales the same architecture toward 576-GPU NVLink domains; Feynman, with the Rosa CPU, follows. Generation by generation, our estimate of the rack dollar shifts the same way: compute's share falls from roughly 43% under Blackwell toward ~31% by Feynman — not because GPUs get cheaper, but because everything required to keep them utilized grows faster. Total memory rises from ~29% toward ~39% (HBM alone from 18–24% toward as much as 23–32%, with Micron already in volume production of HBM4 for Vera Rubin), and the network stops being an accessory: at NVL576 scale it is effectively part of the processor. An accelerator waiting for memory or network traffic is stranded capacity — so the spending migrates to wherever the bottleneck sits.

The geographic consequence compounds this letter's thesis rather than diluting it: Asia's share of the physical system bill rises from roughly 45–50% under Blackwell toward 50–57% with Vera Rubin and possibly 53–60% beyond — Taiwan and Korea strongest, Japan and Malaysia moderate, China flat-to-declining under export controls and diversification, while the US keeps the design, IP and system margin. The next hardware cycle becomes progressively less a pure GPU cycle and more a memory-plus-network-plus-power cycle. For the book, that reads as confirmation rather than adjustment: the two legs and the memory tilt sit where the coming generations push the dollar.

Next week is loaded. Tuesday carries June CPI at 8:30 and the big-five bank kickoff (JPMorgan, Goldman, Citi, Wells Fargo, BofA) in the same morning; ASML reports Wednesday — the first major semiconductor-equipment print of the season, straight into the washout debate; TSMC's monthly sales land the same week. For a global book, ASML is the one to watch — it is Europe's leg of the very pipeline this letter maps: the equipment layer that Taiwan's and Korea's expansion capex flows into.

The three bellwethers. TSMC, ASML, and Korea — where the Korea read is now directly tradable as SKHY rather than only through EWY, which makes the signal cleaner. TSMC's stack remains constructive, ASML is Wednesday's question, and SKHY has no moving averages yet: its only line is $149.

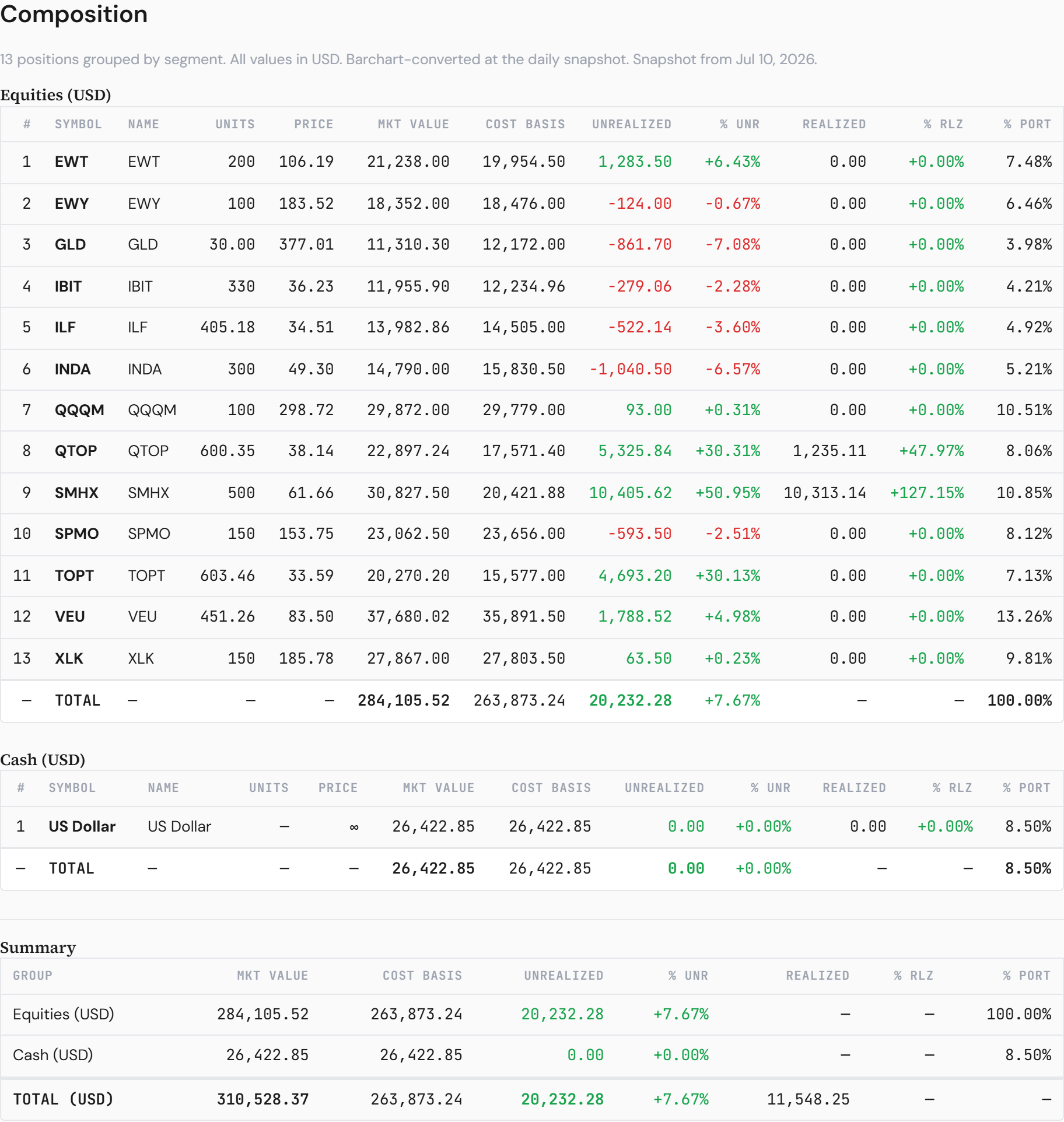

5 · The ETF Portfolio — Global ETFs

What we did this week. Friday's session rebuilt the book — twenty-two lines became thirteen. The full accounting is in Saturday's Daily Pulse (One Core, Three Countries); the short version follows this letter's spine. One broad ex-US core — VEU, doubled to 451 units — per our ETF return-skew work: hold the wrapper that captures the index move, drop the drawer of overlapping slices (both broad EM wrappers, ASEAN, the developed Pacific, ex-US small-caps, the materials sleeve and three micro-thematics all left). The deliberate exceptions sit where the capex dollar lands: Korea opened (EWY), Taiwan increased (EWT), fabless semiconductors increased (SMHX). India was added as the mean-reversion laggard outside tech. US technology is owned at the index level — XLK, QQQM (a pure cost swap from QQQ), QTOP, TOPT — without single-name or subsector bets, and the momentum sleeve (SPMO) stays for as long as the regime reads bull market. Gold, bitcoin and Latin America were untouched. One honesty flag from the log: ASEA's midweek "increase" was a semi-annual distribution reinvesting, not an add — the position was closed Friday.

What we plan to do. Nothing until the tape argues. Two watch-items: whether the periphery's week becomes a month — that would justify a second mean-reversion satellite alongside India — and whether Korea's rest stays orderly. The momentum sleeve survived the whipsaw week; the regime still reads bull market, so it stays.

6 · What May Go Wrong

Three ways this letter's map misleads us. One: the debut fades. SKHY closed 13% over the offer but below its open; under $149 the demand narrative inverts, and with it the cleanest evidence that the Korea discount closes by access. Two: CPI runs hot into an oil bid. Energy just led the sector board; a hot Tuesday print plus firm crude is the rate-path scenario that hits an ex-US channel trading near its upper rail. Three: the flow stays concentrated. The same table that makes Taiwan and Korea the winners makes the ex-US bull a two-country, one-listing bet — and the pool itself is guidance, not contract. If the $675 billion capex midpoint gets cut, Asia's $235 billion is the first line to shrink.

7 · Knowledge Corner

What an ADR actually is — and what a "Korea discount" is. This week's event makes the knowledge piece choose itself. An American Depositary Receipt (ADR) is a US-listed certificate representing shares of a foreign company — SK Hynix's ADRs each represent one-tenth of a Seoul-listed common share, trade on Nasdaq in dollars, and settle like any US stock. Companies list ADRs less for the money (SK Hynix funds its capex from cash flow) than for access: the deepest capital pool in the world, index eligibility, and the governance signal that a US listing sends.

Which is where the second term comes in. The Korea discount is the long-observed tendency of Korean companies to trade below global peers with comparable fundamentals — attributed to chaebol governance structures, capital-return practices that lag developed-market norms, and simple access-and-familiarity friction for foreign funds. The live number this week: SK Hynix at roughly 4.8x forward earnings against Micron's ~6.6x and an industry median near 30x — for the company that leads the segment most levered to AI demand. Both stocks are up roughly 240–250% this year, and the gap barely moved — which tells you the discount is structural, not a performance story. Friday's listing is the first live test of whether direct US access narrows it. Watch the ratio, not the price: if the ADR-to-Micron multiple gap compresses over the coming quarters, the discount was friction; if it persists, it is governance — and priced correctly. Full definitions: Korea Discount · ADR · the full trio anatomy in Three Ways to Own the Memory Supercycle.

8 · Final Words

Valuation gaps do not close by argument; they close by access. This week the market built a door — and the flow framework says what stands behind it. Of every $100 the hyperscalers spend, about $35 lands in Asia. Of every $100 that becomes an AI rack, nearly $80 goes to memory and compute. A US capex boom, a Taiwanese foundry boom and a Korean memory boom are not three stories; they are three accounting views of the same dollar — and the rack roadmap tilts that dollar further toward memory, networks and Asia with every generation. Our book now holds the map rather than a forecast — the core, the two legs, one laggard — and the ratios, not the headlines, will tell us whether the door gets used. Probability, not prophecy.