Closelook@Hypergrowth

The Rotation Got Its Receipts

Last week the flow deltas said the baton was passing — this week IBM, the cyber records and our own indices printed the proof

Current edition · 2026-07-15

This week's edition of Closelook@Hypergrowth, dated July 15, 2026.

Last edition's thesis was stated plainly enough to be wrong: the absolute flow scores still crowned the semiconductors, but the rate of change said leadership was already passing — from the build-out core to the opex layer and the applications. One week later the tape produced receipts. IBM pre-announced a miss and fell 25% in a day — the steepest drop in decades — for exactly the two reasons this letter tracks: memory costs eating legacy IT budgets, and AI spend cannibalizing the incumbents. On the same tape, the AI-opex layer set records: CrowdStrike up 12% and Okta up 11% to new highs, the whole security line green, Cloudflare closing at a record through its 280 line. The software index barely moved while an 18-point spread opened inside it. That is not a market getting risk-off about software. That is a market re-sorting who owns software's future — precisely the hand-off the deltas flagged. The read below updates every tell we named, takes this morning's ASML print into the frame, and gives the earnings season's referee metric — the Earnings Dispersion Ratio — the treatment we promised. The schedule of our other publications is at the end.

1 · This Week's Action

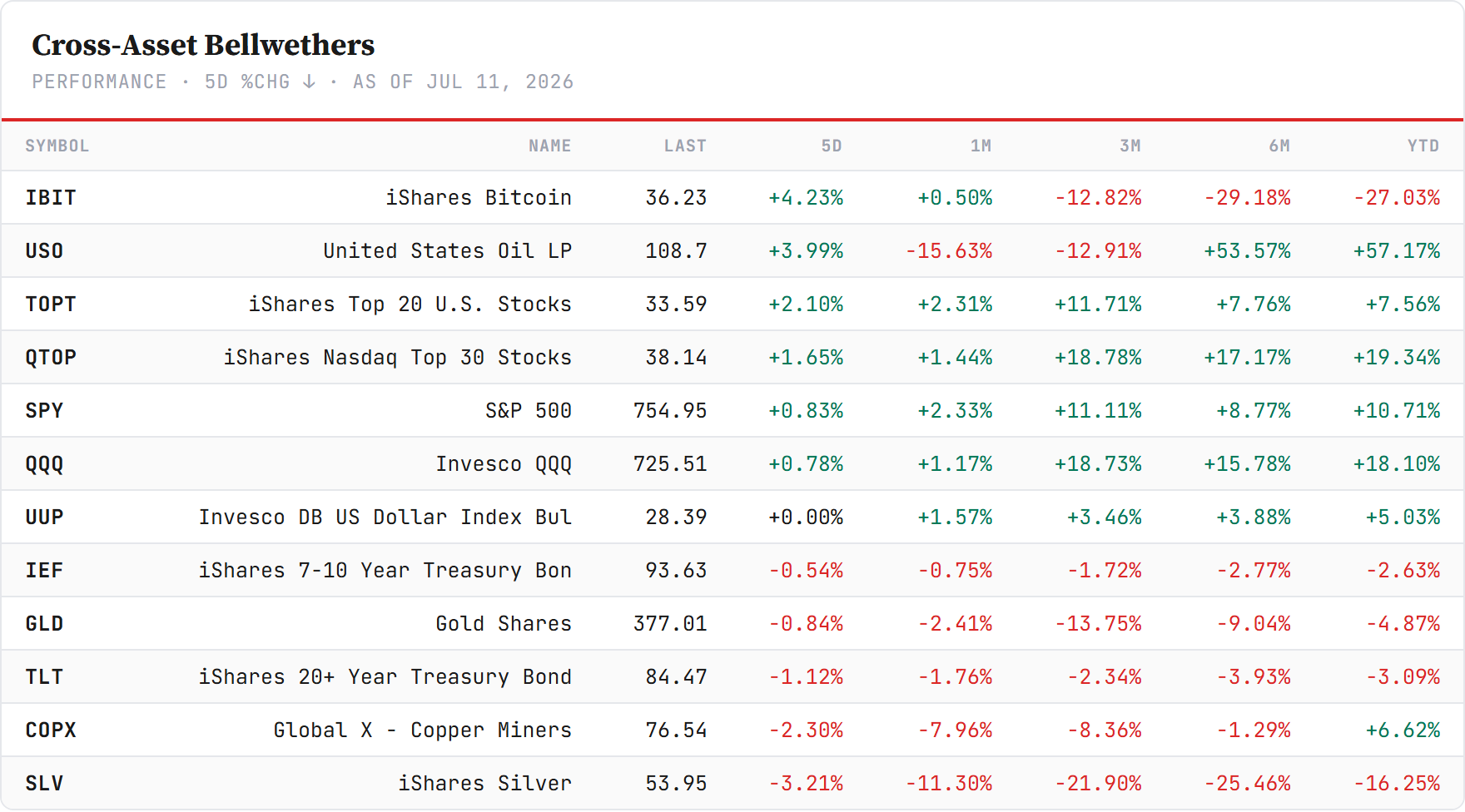

The cross-asset backdrop. June CPI printed a 0.4% monthly decline against a consensus −0.2%, taking the annual rate to 3.5% from 4.2% — and the day after held the move instead of fading it: volatility compressed toward its 52-week low, gold firmed, growth led value again. No haven bid, expectations re-anchoring — the friendliest possible macro floor under a rotation.

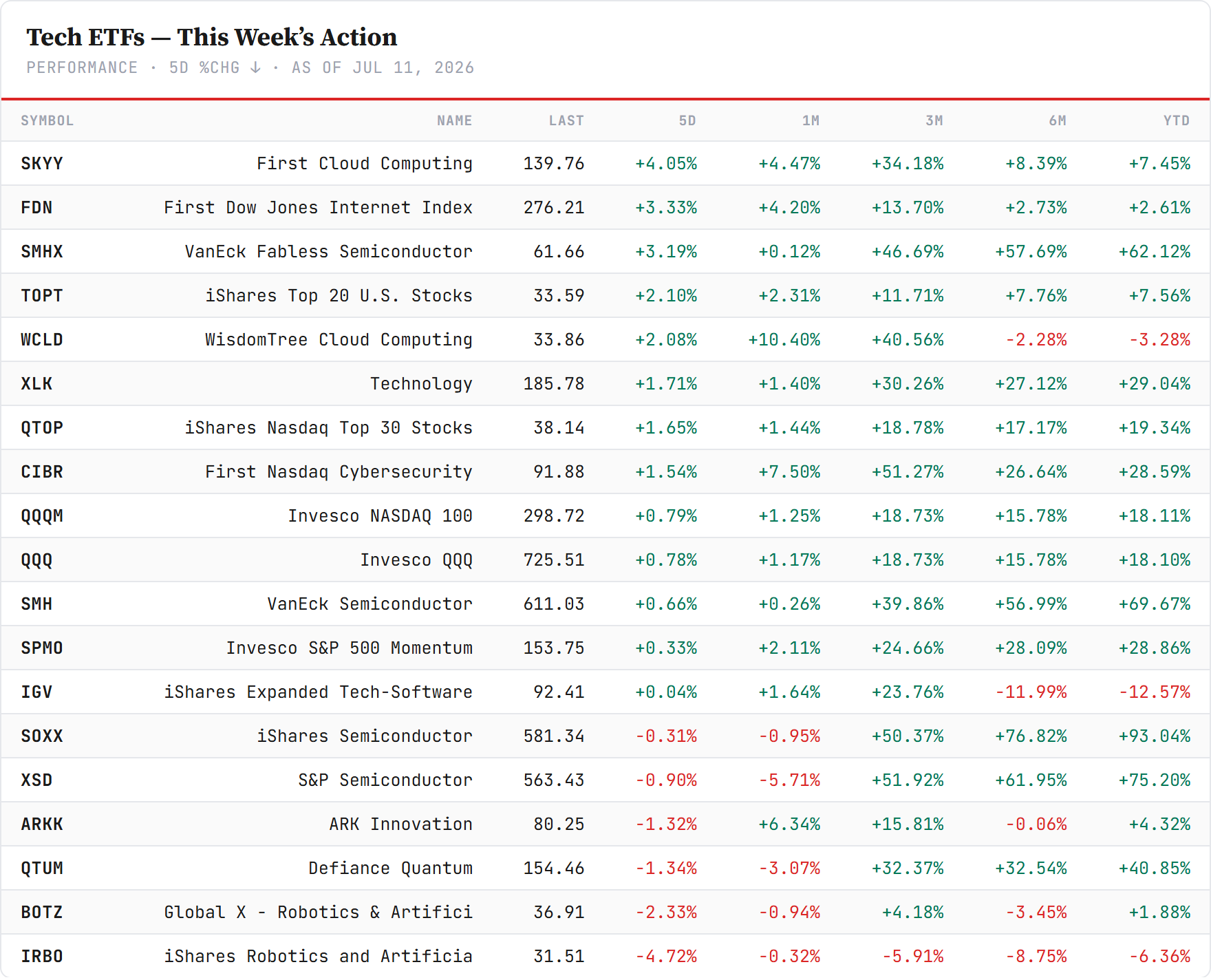

The tech shelf. Two days that belong in a textbook: Monday the semi complex fell 4–5% while software held green — SOXX closing forty cents below the 554 line — and Tuesday the complex reversed hard, SOXX +2.6% back to 567.92, SMH reclaiming 600, with the epicenter itself producing the violence: SK Hynix from two dollars above its $149 offer price to a post-debut high, up 27% in one session, on hard news — 12-layer HBM4 in mass production and shipping to Nvidia. The shelf's message: the washout was positioning, not thesis.

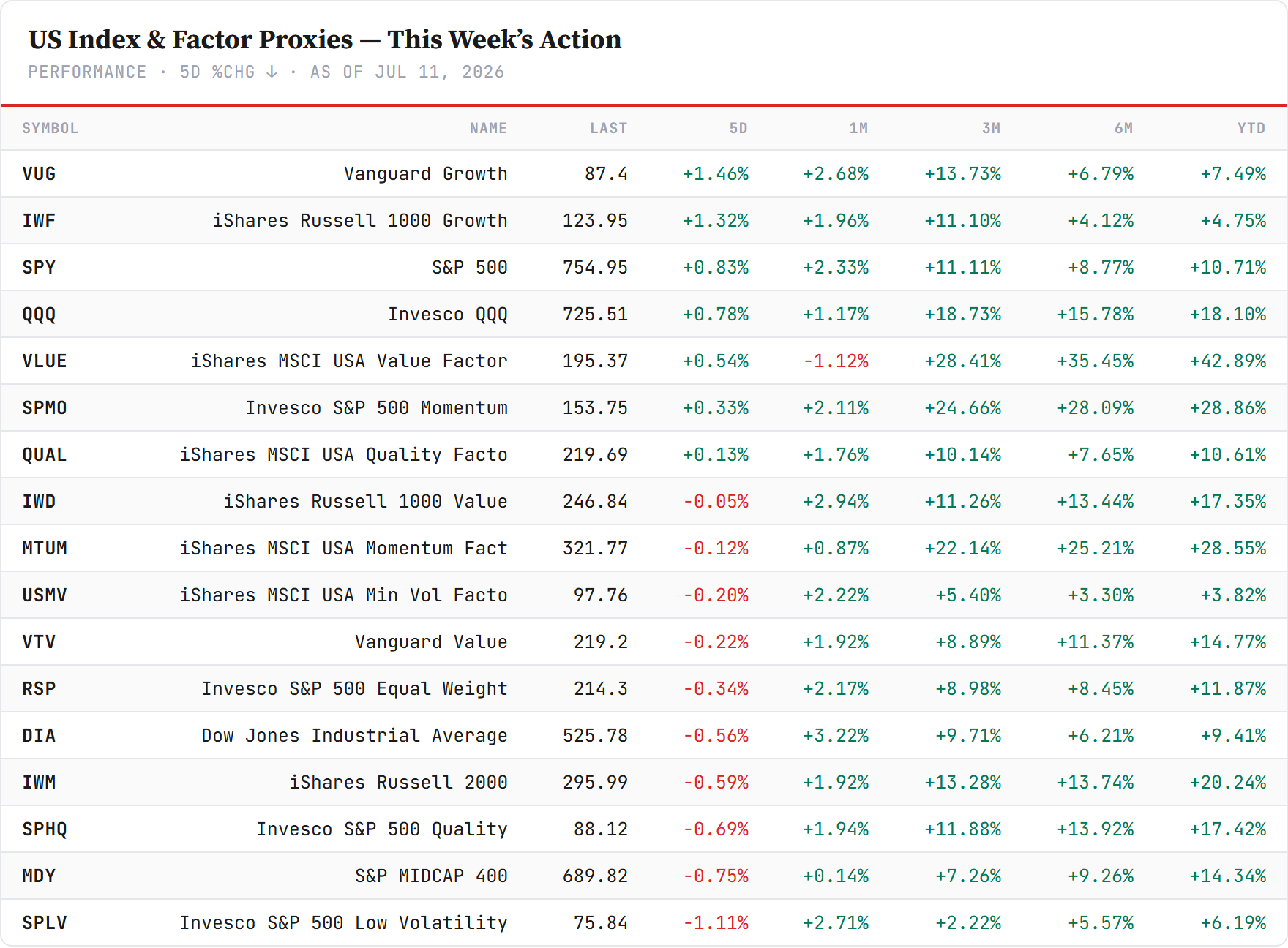

The factor view. The same re-sort one level up: the growth complex caught its bid back, but the year-to-date column still shows the concentration story — the growth factor carried by an ever-narrower list. Hold that thought; it becomes the EDR section below.

Our own board, updated — and the tells resolved. The Rotation Ledger below is the Closelook Directional Flow scan across all four growth buckets, sorted by the 21-day flow delta. Read it against last week's version and every tell we named has an answer:

Three resolutions worth naming. The opex persistence held: a second consecutive week with AI-opex the strongest advancing bucket — the security-and-observability cluster (Fortinet, Palo Alto, Datadog, now Okta and CrowdStrike with them) exactly where we said to watch it. The reversal cluster grew: eighteen of forty agentic winners now flash "reversing-up," from sixteen — and the bellwether row converted: Duolingo's 21-day delta is now +44 with flow still deeply negative, the textbook shape of a destroyed name being re-accumulated. And the one warning fired too: KLA — last week's "single number to watch" — rolled from "stalled" to "accelerating down," the most negative delta in the scan by a factor of three. One core equipment name is repricing, not resting. The complex bounced without it.